PMEGP(Prime Minister's Employment Generation Programme)

It is a credit-linked subsidy scheme launched by the Government of India to promote entrepreneurship and generate employment opportunities in the country, particularly in the micro-enterprise sector. The program is administered by the Ministry of Micro, Small & Medium Enterprises (MSME).

Eligibility:

- Any individual, above 18 years of age

- There will be no income ceiling for assistance for setting up projects under PMEGP.

- For setting up of project costing above Rs.10 lakh in the Manufacturing sector and above Rs. 5 lakhs in the

Service/ Business sector, the beneficiaries should possess at least VIII standard pass educational qualification.

- Assistance under the scheme is available only for new viable projects sanctioned specifically under the PMEGP.

- Existing Units and the units that have already availed any Government Subsidy (under PMRY, REGP,

PMEGP,CMEGP or any other scheme of Government of India or State Government) are not eligible.

- Projects without Capital Expenditure (Term Loan) are not eligible.

- Cost of Land can not be covered under the project cost.

- All Implementing Agencies (KVIC, KVIB, DIC and Coir Board) can process applications in both rural as well as urban

- Applicant should possess valid Aadhaar Number.

- Applicant shall give his/her consent to authenticate demographic details such as Aadhaar number, Name,

Gender, Date of Birth and Mobile number from UIDAI server.

Documents required

- Passport Size Photo

- Highest Educational Qualification

- Project Report Summary/ Detailed Project Report

- Social/ Special Category Certificate, if applicable

- Rural area certificate if applicable

Steps

- Check your eligibility

- Validate/ Authenticate Aadhaar details online

- Generation of User ID and Password that shall be sent through SMS to the registered mobile number of the applicant.

- Login to PMEGP portal to fill further details

- Upload the required documents

- Fill up the Score Card and verify details

- Final Submission

Applicant can track the status of application form submission till final disbursement and adjustment of MM subsidy.

Maximum Project cost for 1 st loan

Rs.50.00 lakhs for manufacturing unit and Rs.20.00 lakhs for Service Unit.

(i)For setting up of new micro enterprise (units)

| Categories of beneficiaries under PMEGP (for setting up of new enterprises) |

| Area (location of project/unit) |

| General Category |

| Special Category (including SC,ST,OBC, Minorities,Women, Ex-Servicemen, Transgenders, Differentlyabled,

NER,Aspirational Districts, Hill and Border areas(as notified by the Government) etc. |

(ii) 2nd loan for upgradation of existing PMEGP/REGP/MUDRA units

- Categories of beneficiaries under PMEGP (for upgradation of existing units)

- All Categories

Maximum Project cost for 2nd loan

Rs.100.00 lakhs for manufacturing unit and Rs.25.00 lakhs for Service Unit.

CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises)Scheme

The Ministry of Micro, Small & Medium Enterprises (MSME) launched the Credit Guarantee Scheme (CGS) in order to improve

the credit delivery system in the country and streamline the flow of credit to the Micro and Small Enterprise (MSE) sector.

CGS-I for Banks/FIs

CGTMSE created a scheme for the provision of guarantees for credit facilities extended by lenders to MSE borrowers.

The scheme was named Credit Guarantee Fund Scheme for Small Industries (CGFSI).

Credit facilities eligible under the scheme

CGTMSE will cover the fund-based and non fund-based credit facilities extended by Member Lending Institutions (MLIs) to MSE borrowers.

These credit facilities can be term loans or working capital loans with the following limits:

| Not more than Rs.50 lakh |

Regional Rural Banks and some financial institutions, micro finance institutions |

| Not more than Rs.200 lakh |

Small Finance Banks (SFBs) and Scheduled Urban Co-operative Banks (including Non-Scheduled Urban Cooperative Banks, State Co-operative Banks and District Central Co-operative banks) |

| Not more than Rs.500 lakh |

Public Sector Banks, Private Sector Banks, Foreign Banks, some Financial Institutions |

A new Hybrid Security product has also been launched by CGTMSE wherein the MLIs can get collateral security for a portion of the credit facility

while the remaining unsecured part will be covered by CGS-I.

This unsecured portion can go up to Rs.200 lakh. It should be noted that CGTMSE will have pari-passu charge on the securities provided.

Credit facilities not eligible under the Scheme

1.Any credit facility in respect of which risks are additionally covered under a scheme operated / administered by

(i)Deposit Insurance and Credit Guarantee Corporation or the Reserve Bank of India

(ii)general insurer or any other person or association of persons carrying on the business of insurance,guarntee or indemnity to the extent they are covered.

(iii)NCGTC Ltd.

2.) Any credit facility, which does not conform to, or is in any way inconsistent with, the provisions of any law, or with any directives or

instructions issued by the Central Government or the Reserve Bank of India, which may, for the time being, be in force.

3.) Any credit facility granted to any borrower, who has availed himself of any other credit facility covered under this scheme or

under the schemes mentioned in clause (i), (ii), (iii) and (iv) above, and

where the lending institution has invoked the guarantee provided by the Trust or under the schemes mentioned in clause (i), (ii), (iii) and (iv) above

but has not repaid any portion of the amount due to the Trust or under the schemes mentioned in clause (i), (ii), (iii) and (iv) aboveas the case may be, by reason of any default on the part of the borrower in respect of that credit facility

4.) Any credit facility which has been sanctioned by the lending institution

against collateral security and / or third party guarantee.

However, after the introduction of Hybrid Security model, MLIs can cover the unsecured part of the credit facility(ies) under CGTMSE upto the overall

exposure of ₹500 lakh.

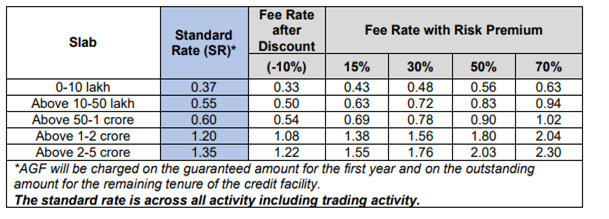

Annual Guarantee Fee (AGF)

AGF is charged on the guaranteed amount for the initial year, and on the amount outstanding for the rest of the tenure. The AGF structure is as follows:

Extent of the Guarantee Coverage

| Category |

Maximum extent of Guarantee where credit facility is |

|

|

|

Up to Rs.5 lakh |

Above Rs.5 lakh and up to Rs.50 lakh |

Above Rs.50 lakh and up to Rs.5 crore |

| Micro Enterprises |

85% |

75% |

75% |

| MSEs located in North East Region (incl. Sikkim, UT of Jammu & Kashmir & UT of Ladakh) |

80% |

|

|

| Women entrepreneurs / SC/ST entrepreneurs / Person with Disability (PwD)/ MSE promoted by Agniveers / MSEs situated in Aspirational District / ZED certified MSEs |

85% |

|

|

| All other category of borrowers |

75% |

|

|

The AGF is usually paid to the Trust by the institution receiving the guarantee within 30 days of loan disbursal. This payment can be made through NEFT/RTGS

CGS-II for NBFCs

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) has created a scheme for the provision of guarantees for credit facilities

extended by NBFCs to MSE borrowers. The key features of this scheme are as follows:

The Trust will cover loans extended by MLIs to eligible borrowers in the MSE sector. The loan in this case should not be more than Rs.500 lakh.

For MSE Retail Trade, the credit facility coverage will be up to Rs.100 lakh.

The credit facility should be standard and regular as per the RBI guidelines.

The credit facility should not be used for the repayment of debts.

Guarantee Fee

The trust with relation to the credit facilities and extended to the borrower may undertake provided an eligible lending body may provide a guarantee on account of the credit facility.

The trust is within its rights to accept or reject any proposal referred by the lending body provided it satisfies the norms of the scheme.

Standup India Scheme

For financing SC/ST and/or Women Entrepreneurs above 18 years of age.

To facilitate bank loans(Composite loan inclusive of term loan and working capital ) between Rs.10 lakh and Rs.1Crore to at least one Scheduled Caste (SC) or Scheduled Tribe (ST) borrower and at least one woman borrower per bank branch for setting up a only greenfield enterprise engaged in manufacturing, services, agri-allied activities or the trading sector.

(Here green field the first time venture of the beneficiary in the manufacturing or services or agri-allied activities or trading sector).

For non-individual enterprises at least 51% of the shareholding and controlling stake should be held by either an SC/ST or woman entrepreneur.

Borrower should not be in default to any Bank / Financial Institution.

Loan details

- Size: Composite loan of 85% of project cost inclusive of term loan and working capital.

- Exception: The stipulation of the loan being expected to cover 85% of project cost would not apply if borrowers contribution along with convergence support from any other schemes exceeds 15% of the project cost.

- Interest rate : Lowest applicable rate of bank for that category not to exceed MCLR (base) rate of the bank + 3% + Tenure Premium.

- ecurity : Besides primary security, the loan may be secured by collateral security or guarantee of Credit Guarantee Fund Scheme for Stand-Up India Loans (CGFSIL) as decided by the banks.

- Repayment : With in 7 Years with a maximum moratorium period of 18 months.

- Withdrawal of Working capital : Upto 10Lakhs –Sanctioned by way of Overdraft. Rupay credit card will be issued & above 10Lakhs –Sanctioned by way of Cash credit limit.

- Margin Money : 15% margin money which can be provided in convergence with eligible central/state schemes. The borrower shall be required to to bring in minimum of 10% of Project cost as Own contribution.

Central Subsidies

- Skill Upgradation& Quality improvement and Mahila Coir Yojana (MCY)

- Trade-Related Entrepreneurship Assistance andDevelopment (TREAD)

- Subsidised term loan

- Swachhta Udyami Yojana (SUY)

- Special Credit Linked Capital Subsidy Scheme (SCLCSS) for MSEs under National Scheduled Castes and Scheduled Tribes Hub Scheme-reg

- Amended Technology Upgradation Fund Scheme(ATUFS)

- Integrated Development of Leather sector (IDLS) Scheme

- Credit Linked Capital Subsidy Scheme for Technology Upgradation (CLCSS)

- Quality Upgradation Support for MSMEs (TEQUP)

- Government Subsidy for Small Business for Cold Chain

- Extensionof Financial Assistance to Coir units in the Brown Fibre sector

- Scheme for Extension of Financial Assistance for Generator Set / Diesel Engine

- Marketing Assistance Scheme by NSIC

- ISO 9000/ISO 14001 Certification Reimbursement Scheme

- Marketing support/Assistance to MSMEs (Bar code)

- Support for Entrepreneurial and managerial development of SME

- Lean Manufacturing competitiveness schemes for MSMEs

- Prime Minister Employment Generation programme (PMEGP)

- Scheme for Integrated Textile Parks (SITP)

- In-situ Upgradation of Plain Power looms

- Group Work shed Scheme (GWS)

- Yarn Bank Scheme

- Common Facility Centre (CFC)

- Pradhan Mantri Credit scheme for Power loom Weaver

- Solar Energy Scheme for Power loom

- Grant-in-Aid and Modernisation & Upgradation of Power loom Service Centres (PSCs

- Modified Comprehensive Power Loom Cluster Development Scheme (MCPCDS)

- Integrated Processing Development Scheme (IPDS)

- SAMPADA (Scheme for Agro-Marine Processing and Development of Agro Processing Clusters

- Market Development Assistance Scheme for Micro/ Small manufacturing enterprises/ Small & Micro exporters (SSI-MDA)

- Micro & Small Enterprises – Cluster Development Programme (MSE-CDP

- Digital MSME†Scheme for promotion of Information and Communication Technology (ICT) in MSME Se

- Support for Entrepreneurial and Managerial Development of SMEs Through Incubato

- Financial Support to MSMEs in ZED Certification Scheme

- Design Clinic for Design Expertise to MSMEs

- Enabling Manufacturing Sector to be Competitive through QMS&QTT

- Building Awareness on Intellectual Property Rights (IPR)

- Coir Vikas Yajna (CVY)

- Scheme for Technology Upgradation/ Establishment/ Modernization for Food Processing Industri

- Ministry of Micro, Small and Medium Enterprises, Govt, of India

- Science and Technology (S&T) for Coir Institutions

- Market Promotion & Development Scheme

- Domestic Market Promotion (DMP)

- A Scheme for promoting Innovation, Rural Industry & Entrepreneurship (ASPIRE)

- International Cooperation

- Procurement and Marketing Support Scheme (P&MS)

- Support for Entrepreneurial and Managerial Development of MSMEs through Incubators

- Performance & Credit Rating Schem

- Coir Udyami Yojana